Introduction

In case of GST, tax is payable on ad-valorem basis i.e., percentage of value of the supply of goods or services. Thus, it becomes important to know how to arrive at the value on which tax is to be paid. Section 15 of the CGST Act prescribes the provisions for determining the value of supply of goods and services made in different circumstances and to different persons.

Example 1: Transaction Value

An Advertising Agency provides service to his client Mohan under a contract with fees of Rs. 18,000. Mohan makes payment in 2 instalments with a gap of a month. In addition to this, agency incurred travelling expense for the sum of Rs. 2,000 which is reimbursable by Mohan.

Hence, despite the payments were made in instalments, the price to be paid by Mohan is Rs. 20,000. And the Transaction Value of this transaction will be Rs. (18,000+2,000) = Rs.20,000.

Example 2: Payment mode

In above example 1, if Mohan makes payment of one instalment through Person X from whom, Mohan is liable to receive money.

Still, Transaction Value of the transaction remains Rs. 20,000 only.

This is because, any direct or indirect payment made by recipient to the supplier will be part of transaction value.

Example 3: Taxes

Mr. X purchased a car of list price Rs. 5,50,000 along with Road Tax costs Rs. 50,000. GST is liable at applicable rate on the value of Rs. 6,00,000. This is because transaction value includes all the taxes so incurred except taxes under GST Act.

Example 4: Free Gifts/ Volumes Incentives /Free Trips

It can be bifurcated into two categories:

Category 1 – Transactions related to the Sales.

Category 2 – Transactions unrelated to Sales.

In case of Category 1, when Gold Coins are given as incentives on fulfilment of agreement then, ITC need not be reversed as it does not partake the nature of a gift since it was related to sales

However, with respect to Category 2, when the goods are supplied without any obligation then credit may not be availed in such case according to section 17(5) of CGST Act.

Example 5: Incidental Expenses

Priya purchased a dress for Rs. 7,500 from a shop. She asked for a shopping bag which costs Rs. 50. While calculating GST, charges for shopping bag must be considered, i.e. Transaction Value will be Rs. 7,550, because incidental charges related to the value of supply must be taken while deriving at Transaction Value.

Example 6: Penalty, interest or late fees

Honda Company sold a car for Rs. 9,00,000 to Mr. Ramesh. Ramesh agreed to the terms and conditions and as per the agreement and he was liable to pay the amount on or before 15/05/2020. But he failed to pay and paid the amount on 25/05/2020. Due to violation, Honda Company charged Rs. 50,000 with regard to penalty on delayed payment. Therefore, as per sec 15(2)(d), Transaction Value will be Rs. 9,50,000 which includes penalty amount also.

Example 7: Treatment of TCS under Income Tax Act

The CBIC vide Circular No. 76/50/2018 GST dated 31.12.2018 (amended vide corrigendum dated 7.03.2019) has clarified that for the purpose of determination of value of supply under GST, tax collected at source (TCS) under the provisions of the Income Tax Act, 1961 would not be includible as it is an interim levy not having the character of tax.

Example 8: Subsidy Summary

Example 9: Discounts

Mr. P, a trader provides the following information in his invoice dated 9.11.2019.

Particulars | Amount (Rs.) |

Supply of 200 pieces of skirts of different colours at the rate of Rs. 800 per piece | Rs. 1,60,000 |

Discount 20% | Rs.16,000 |

Net amount payable | Rs. 1,44,000 |

In this case, the value of supply of goods shall be Rs. 1,44,000.

Example 10: Discounts

In case of discount by way of credit note.

During such cases, discount given by issuance of credit note to the dealer is under an agreement entered at the time of supply of goods and thus such discount shall not form value of supply provided input tax credit has been reversed by such dealer to whom credit note was issued, of the supply as is attributable to the discount on the basis of credit note issued by the supplier.

Example 11: Staggered Discounts

Offer says that Purchase on and above Rs. 5000 gets a discount of 10% of invoice value itself. As per 15(3), such discount is excluded from Valuation of Supply.

Example 12: Periodic/ Volume Discounts

Offer says additional discounts of 1% if customer purchase above Rs. 10,000 and increases by 1% with increase in purchase of Rs. 10,000. Since such discounts are at or before the time of supply and not based on actual quantum hence discounts are passed through credit notes. As per 15(3), such discount is excluded from Valuation of Supply.

Example 13: Secondary Discounts

X supplies to Mr. Y 40,000 packets of Maggi at Rs. 10. After sale, Mr. X revalue the Cost at Rs. 8.

Hence, Mr. X issues a credit note with respect to it.

Therefore, secondary discounts shall not be included in the Transaction Value.

Example 14: Buy one, Get one Free Discounts

Westside monsoon sale is going on and they announce their offer of “Buy 1, Get 1 Free” which means if a person wants to buy 2 shirts worth of same price then that person is liable to pay the price equal to one product only and hence such discount are excluded from Transaction Value.

When the Transaction Value is not assessable value if Supplier and Recipient are RELATED or Price is not sole consideration or transaction is not reliable. In such cases, Valuation is to be done on the basis of “VALUATION RULES”.

Rule No: | Details |

27 | Value of supply when consideration is not wholly in money |

28 | Value of supply when made other than through an Agent |

29 | Value of supply when made through an Agent |

30 | Value of Supply based on Cost |

31 | Value of Supply through Residual Method |

31A | Value of Supply in case of Gambling, Lottery and Horse Race |

32 | Value of Supply in Certain Supplies |

32A | Value of Supply in case of Kerala Food is Applicable |

33 | Value of Supply in case of Pure Agent |

34 | Value of supply in case of rate of Exchange of Currency other than Indian Rupees |

35 | Value of Supply inclusive of IGST, SGST, CGST and UTGST |

RULE 27: Determination of value when consideration is not wholly in money

Where the supply of goods or services is for a consideration not wholly in money, the value of the supply shall, –

Example 15: Rule 27

Laxman Purchase a mobile phone having Open Market Value of Rs. 30,000 from Ram, in exchange of his old phone. The cost of Old Phone is Rs. 3,000. Hence, Ram agreed the transaction at Rs. 27,000.

Despite of Laxman actually paying Rs. 27,000 the Transaction Value of the supply is Rs. 30,000 as stated in rule 27 of GST Act.

RULE 28: Value of supply of goods or services or both between distinct or related persons, other than through an agent

The value of the supply of goods or services or both between distinct persons (same entity) as specified in sub-section (4) and (5) of section 25 or where the supplier and recipient are related, other than where the supply is made through an agent, shall-

Provided

Example 16: Rule 28

Mr. Ram, proprietor of Sri Krishna Manufactures supplied certain goods costing Rs. 75,000/- to its employees at Rs. 60,000/-. In such a case, as both the assessee and its employee come under the definition of related parties under the GST Act, open market value as per Rule 28 if available will be applicable. The open market value of the goods were Rs. 75,000/- which would constitute to be the value of supply in such a case.

Rule 29: Value of supply of goods made or received through an agent

The value of supply of goods between the principal and his agent shall, –

Example 17: Rule 29

Where a principal supplies groundnut to his agent and the agent is supplying groundnuts of like kind and quality in subsequent supplies at a price of Rs.5,000 per quintal on the day of supply. Another independent supplier is supplying groundnuts of like kind and quality to the said agent at the price of Rs.4,550 per quintal. The value of the supply made by the principal shall be Rs.4,550 per quintal or where he exercises the option the value shall be 90% of the Rs.5,000 i.e. is Rs.4500 per quintal.

Rule 30: Determination of Value of Supply Based on Cost

Where the value of a supply of goods or services or both is not determinable by any of the preceding rules,

the value shall be 110% of the cost of production or manufacture or cost of acquisition of such goods or cost of provision of such services

Example 18: Rule 30

ABC Ltd. manufactures table at Rs. 5,000 as further sell to PQR Ltd. The Open Market Value of the same table is Rs. 7,000. Since the open market value is known to us hence the Value of supply will be Rs. 7,000. Whereas, the open market value is not determinable, the value of supply will be 110% of Cost of Production. That is, Rs. 5,500 (110% * 5000) as per Rule 30 of GST Act.

Rule 31: Determination of Value of Supply Through Residual Method

The value of supply of goods or services or both can be determined using reasonable means consistent with the principles and general provisions of section 15 and these rules.

Rule 31A: Determination of Value of Supply in case of Lottery, Gambling and Horse Race

Note: Lottery run & authorised by SG means- A lottery not allowed to be sold in any state other than the originating state.

Value of supply of actionable claim in the form of chance to win in betting, gambling or horse racing in a race club shall be 100% of the face value of the bet or the amount paid into the totalisator.

Rule 32: Determination of Value of Supply in Certain Supplies

(1) Notwithstanding anything contained in the Act or in these rules, the value in respect of supplies specified below shall be determined in the manner provided hereinafter.

(2) The value of supply of services in relation to purchase or sale of foreign currency, including money changing, shall be determined by the supplier of service in the following manner:

(3) The value of supply of services in relation to booking of tickets for travel by air provided by an air travel agent,

(5) Where a taxable supply is provided by a person dealing in buying and selling of second hand goods

Where ITC is not availed on such purchase of goods, Value of Supply will be (selling price – purchase price) and in case of negative you need to ignore.

(6) The value of a token, or a voucher, or a coupon, or a stamp (other than postage stamp) which is redeemable

Money value of the goods or services or both redeemable against such token, voucher etc.

(7) Notified services between distinct persons without consideration

Value = Nil, if ITC is available

Example 20: Rule 32(2)(a) Hawaii Ltd sold 20,000 units of USD. Conversion rate is 1 USD = Rs. 60 As per RBI Reference rate, it is USD 1 = Rs. 59 Value of Supply: Rs. (60-59) * 20,000 = Rs. 20,000. |

Example 19: Rule 32(5)

Mr. Honey a dealer in second hand cars, purchase the cars and sells them after painting and some repair. He does not take credit of any of the purchases. He sold one car at Rs. 90,000 which was purchased by him at Rs. 85,000. In the above scenario, value of supply would be Rs. 90,000-85,000 = Rs. 5000/-.

However, if in the above scenario, the purchase price would have been above 90,000 Rs, value of supply would be Nil.

In case where the RBI reference rate for a currency is not available, the value shall be 1% of the gross amount of Indian Rupees provided or received by the person changing the money.

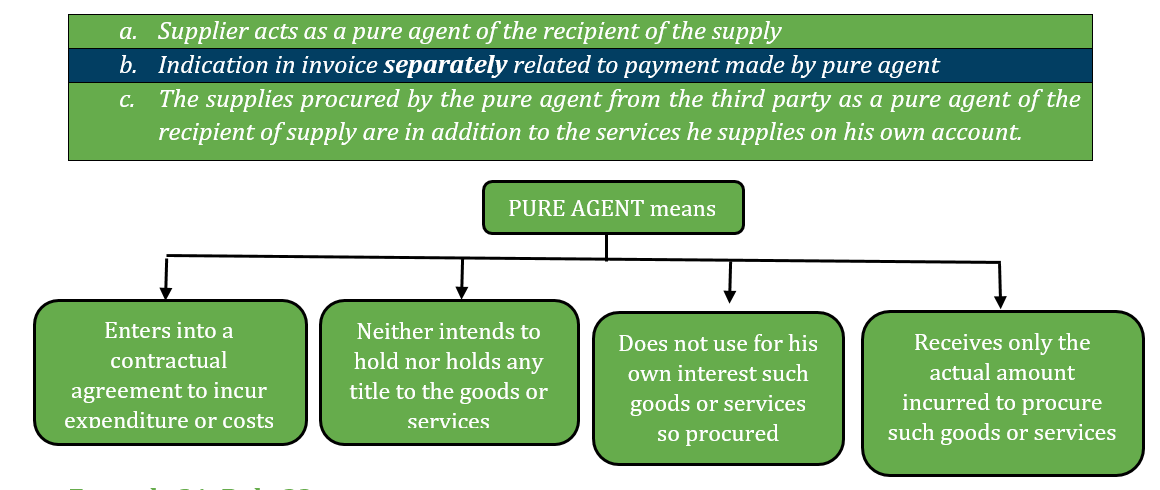

Rule 33: Determination of Value of Supply in case of Pure Agent

Notwithstanding anything contained in the provisions of this Chapter, the expenditure or costs incurred by a supplier as a pure agent of the recipient of supply shall be excluded from the value of supply, if all the following conditions are satisfied, namely, –

Example 21: Rule 33

Corporate services firm A is engaged to handle the legal work pertaining to the incorporation of Company B. Other than its service fees, A also recovers from B, registration fee and approval fee for the name of the company paid to the Registrar of Companies. The fees charged by the Registrar of Companies for the registration and approval of the name are compulsorily levied on B. A is merely acting as a pure agent in the payment of those fees. Therefore, A’s recovery of such expenses is a disbursement and not part of the value of supply made by A to B.

Rule 34: Determination of Value of Supply in case of Rate of Exchange except Indian Rupees.

Rule 35: Determination of Value of Supply Inclusive of Integrated Tax, Central Tax, State tax, Union Territory Tax

Where the value of supply is inclusive of integrated tax or, as the case may be, central tax, State tax, Union territory tax, the tax amount shall be determined in the following manner, namely, –

Tax amount = (Value inclusive of taxes X tax rate in % of IGST or, as the case may be, CGST, SGST or UTGST) ÷ (100+ sum of tax rates, as applicable, in %)

Example 22: Rule 35

If the Value of Supply Inclusive of tax is Rs. 100 and applicable GST rate is 18% then,

TAX AMOUNT = (100*18)/ (100+18) = Rs. 15.25.