INTRODUCTION

Nowadays, Business restructuring has become vital for businesses in quite a few industries today. This is because Covid-19 has impacted them a lot and in order to survive, they are considering business restructuring as a viable option.

A major form of business restructuring is to transfer the business from the existing entity to another entity. This transfer majorly takes place through Amalgamation, Merger, Demerger, etc. Now considering such transfer, it is necessary to understand GST implications of such transfer.

HOW CAN BUSINESS TRANSFER TAKE PLACE?

SLUMP SALE:

As per Sec. 2(42C) of the Income Tax Act, 1961, “slump sale”, means the transfer of one or more undertakings as a result of the sale for a lump sum consideration without values being assigned to the individual assets and liabilities in such sale.

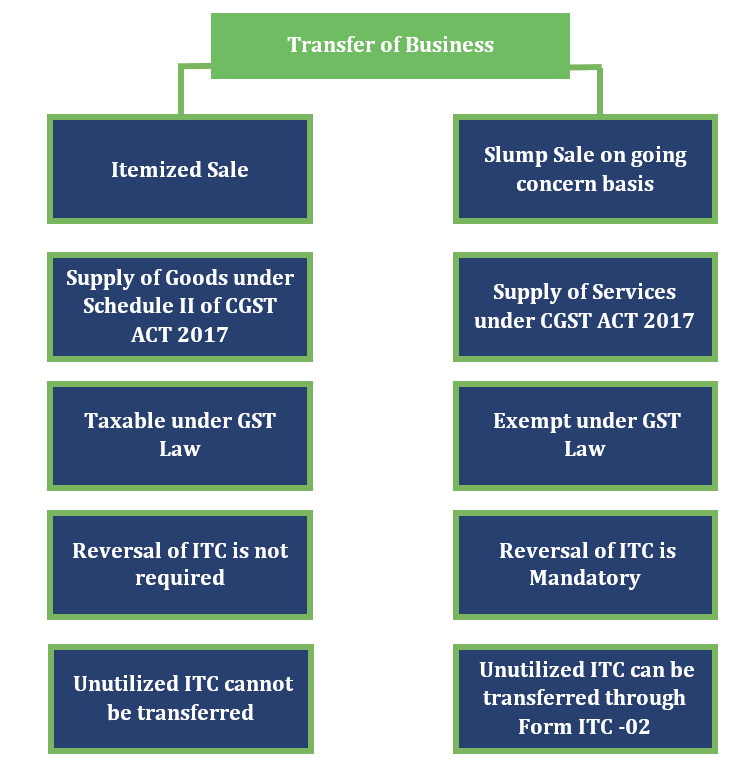

ITEMIZED SALE:

Where values are assigned to each of the assets transferred, then such transfer is called itemized sale.

WHETHER TRANSFER OF BUSINESS IS SUPPLY OF GOODS OR SUPPLY OF SERVICES?

When assets are transferred under itemized sale, the same shall be treated as supply of goods.

However, we need to check the nature of supply when business as a whole is transferred.

The following is the definition of Goods:

In terms of Sec. 2(52) of CGST Act, 2017, “goods mean every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply”.

Therefore, to be called as goods, it has to be movable property. As business cannot be said to be movable, transfer of business cannot be said to be a transfer of goods.

Now, let us find out whether such transfer will be considered as a transfer of service –

In terms of sec. 2(102) of CGST Act 2017, services mean anything other than goods. The term service is wider in its scope. As it covers anything other than goods, transfer of business which cannot be considered transfer of goods will fit into the definition of “service”. Further, in case of the judgment given by Andhra Pradesh High Court in case of Paradise Food Court vs. State of Telangana 2017 VIL 238 AP in the context of VAT Law, it was held that the “business” is not movable property and is, therefore, not goods. Hence, based on the above we can conclude that transfer of business is a service.

WHAT IS THE GST LIABILITY ON TRANSFER OF BUSINESS?

UNDER ITEMIZED SALE

However, an important thing to note here is that in case of Itemized sale, since the assets are assigned values individually, such transfer would be taxable since the business assets are not transferred as a whole.

Further the transfer of business as itemized sale falls under supply of goods in GST and is taxable under Schedule II of CGST Act.

UNDER SLUMP SALE

In case of a slump sale, the business is usually transferred as “Going Concern”.

The Going Concern concept assumes that the business will continue to function in the foreseeable future. The assumption implies that the business would not discontinue its operations in the near future.

Transfer as a Going Concern is considered as exempt under the GST law.

Another Condition for claiming exemption is that the business should be transferred as a separate unit i.e. as an independent part.

NOW LET US UNDERSTAND THE IMPACT OF SLUMP SALE ON INPUT TAX CREDIT IN GST

REVERSAL OF ITC IN CASE OF EXEMPTION

Since transfer of business as going concern is exempt under GST, according to sec. 17 read with rule 42 of CGST Rules, 2017, in case any registered person is having any exempted supplies, then ITC pertaining to such exempted supplies shall be reversed proportionately. So the transferor will have to reverse the ITC taken earlier.

TRANSFER OF ITC

Sec. 18(3) of the CGST Act, 2017 states that, where there is a change in the constitution of a registered person on account of transfer of the business with the specific provision for transfer of liabilities, the ITC which remains unutilized in his electronic credit ledger shall be transferred to the resultant entity.

The registered person can transfer such unutilized credit by filing FORM ITC-02 electronically on the GST portal and such application shall be accompanied by a copy of certificate issued by a practicing

CA or CMA which certifies that the liabilities are also transferred at the time of transfer of business.

Once the above things are done, the transferee shall on the common portal accept the details furnished in Form ITC-02, then the ITC shall be transferred to the transferee’s electronic credit ledger.

LIABILITY OF TRANSFEROR AND TRANSFEREE

In case of any tax liability arises prior to transfer, both the parties i.e. the transferor and transferee will be jointly and severally liable for such liability.

The joint and several liabilities will exist even if such amounts were determined and become due after the transfer of business.

REGISTRATION

The registration aspect is among the most important aspect while considering a transfer business on account of sale, amalgamation, merger, etc.

As per section 22(3) of the CGST Act, when a business is transferred as a going concern (which normally happens by way of slump sale), the transferee is liable to get themselves registered with effect from the date of such transfer.

For example, if company A transfers one of its business to a firm B on 25th Sept, then that firm is liable to get itself registered retrospectively with the GST portal on that day itself i.e. 25th Sept. Hence, it is advised to decide in advance the date of transfer for smooth registration process.

Another method of transferring the business is going through the scheme of amalgamation, merger, etc. Now, here it is important to know that such transfer may happen voluntarily or by an order of a High Court or Tribunal. Such order is normally given when the court is of the opinion that the management is incapable of running the company or in case when the company files bankruptcy. Now, on completion of the scheme, the Registrar of Companies issues an incorporation certificate.

As per Sec. 22(4) of the CGST Act, the transferee is liable to get themselves registered with effect from the date on which the ROC issues the incorporation certificate.

All the transactions by the companies between the effective date of the scheme and the date of approval by the high court or tribunal shall be treated as distinct transactions.

The individual companies shall comply with all the laws in the said period as distinct companies.

Authors

CA Shreyans Dedhia

Partner | shreyans.dedhia@masd.co.in

Anuj Pai

Associate Consultant | anuj.pai@masd.co.in