Introduction:

Determining an appropriate costing of your product can make or break your business. Most business owners fail to understand the importance of costing which can actually help your business avoid running into troubles such as loss of profits, time mismanagement and over budgeting. Knowing how much the company spends to produce a product is not enough when it comes to figuring out the product’s costing value. Furthermore, selling a product with a wrong value can have a great impact on your company’s sustainability. To run a successful business, you need to think ahead against your competitors and one way of doing so is to understand what product costing needs to be followed.

Costing techniques can be tricky and complicated to understand and hence requires a systematic approach in determining the same. This article broadly covers determining the costing in case of Manufacturing industry.

Determining costing in a Manufacturing Industry:

Inventory:

For a manufacturing industry, inventories play a major role because a manufacturer relies on inventory to complete a finished product for which It expects to be paid and hence efficient management of inventory Is the goal of every manufacturer because inventory has a direct impact on profits through an income statement item called Cost of Goods Sold. Here comes the role of Inventory costing.

Inventory costing determines how purchased materials and materials made to stock are priced. Mostly companies will employ one of the following types of inventory costing methodologies:a. First-In, First-Out (FIFO)

– FIFO establishes that the oldest layers of inventory (based on received date or manufacturing date) are used before the newer layers. Most companies employ this method as it is usually a better correlation of material costs associated with a sale.b. Last-In, First-Out (LIFO)-

LIFO establishes that the newest layers of inventory (based on received date or manufacturing date) are used up before the older layers. Few manufacturers employ this method.c. Average or Weighted Average Cost-

Average or Weighted Average essentially establishes that there is only one inventory layer in inventory. That layer is the “average cost” of all the items currently in existence in the inventory pool. Any time a new layer is added to inventory, a new “per unit output price” is computed and applied to any outbound inventory transactionii. Implementation of BOM:

The BOM or the product structure as they call it, is a list of all the raw materials needed to run the manufacturing process. BOM consists of a list of all the items & components needed to manufacture a particular product. Testing of BOM should be first step before finalizing BOM list for finished goods. A solid BOM calls for a healthy business and that’s why it serves as an indispensable part of manufacturing process which must be handled with extreme care.

iii. Production Costing:

There are a number of varying methods of production costing to choose from, each with their own benefits and drawbacks.

Major Production Costing Approaches:

Example:

Pk Limited is newly incorporated in the business of manufacturing of Electrical products. They have 2 Special Product namely one-way Switch and 3 PIN Multiple Plug. On the basis of forecasted sales, Company has decided to produce 7500 units of one-way switch and 2750 units of 3 PIN Multiple plugs, to produce 1 unit of each product they require following raw material and packing material

FG | Type | Particulars | UOM | Qty | Rate (Rs.) |

One-way Switch | Raw Material | Switch Base | No | 1 | 2.60 |

| Raw Material | Wire Screw | No | 4 | 0.60 |

| Raw Material | PG Wire | Cm | 25 | 0.05 |

| Packing Material | Switch Label | No | 2 | 0.40 |

| Packing Material | Outer Box | No | 1 | 0.50 |

3 PIN Multiple Plug | Raw Material | Multi Socket | No | 3 | 4.00 |

| Raw Material | Plug Inner | No | 1 | 2.50 |

| Packing Material | Box label | No | 2 | 0.90 |

| Packing Material | Outer box | No | 1 | 0.60 |

Since the raw material and packing material were purchase during the year company has decided to considered standard costing and have considered rate as mentioned in above table which is including buffering rate (i.e., 5%)

Raw material gets converted into finished goods by passing through 2 stages, each stage is Labour and machine oriented. To produce 500 units of the finished goods required labour hours and machine hours are as below:

Labour cost | Machine Cost | |||||

Type of Labour | Labour Hour | Rate per Hour | Machine hour | Kilowatt per hour | Rate per Kilowatt | |

Un-skilled | 5 | 100 | 8 | 100 | 4 | |

Skilled | 1 | 600 | ||||

Apart from above mentioned cost company has to incurred following variable overheard of 25 Paise per unit and Fixed Overhead as below

Fixed Overhead | Amount (Rs.) |

Factory Rent | 2,50,000 |

Salary | 75,000 |

Repairs and maintenance | 50,000 |

Sundries | 35,000 |

Total | 4,10,000 |

Company also has decided to apportion of fixed overhead in the ratio of quantity produced. Here is how cost per unit is calculated.

Note 1: Apportionment of Fixed Cost

Particular | Qty | Calculation | Amount |

One-way Switch | 7,500 | 4,10,000 x 7500/10250 | 3,00,000 |

3 PIN Multiple Plug | 2,750 | 4,10,000 x 2750/10250 | 1,10,000 |

Total | 10,250 | 4,10,000 |

Note 2: Kilowatt hours

Rate per kilowatt hours = 100 Kilowatt per hour x 4 Per hour

= Rs.400 Per Kilowatt hour

Calculation of cost per Unit

Cost | Bifurcation | Total Cost | |

One-way Switch | 3 PIN Multiple Plug | ||

Raw Material |

|

| |

Switch Base | 7500 x 1 x 2.6 | 19,500 |

|

Wire Screw | 7500 x 4 x 0.6 | 18,000 |

|

PG Wire | 7500 x 25 x 0.05 | 9,375 |

|

Multi Socket | 2750 x 3 x 4 |

| 33,000 |

Plug Inner | 2750 x 1 x 2.5 |

| 6,875 |

Packing Material |

| ||

Switch Label | 7500 x 2 x 0.4 | 6,000 |

|

Outer Box | 7500 x 1 x 0.5 | 3,750 |

|

Box label | 2750 x 2 x 0.9 |

| 4,950 |

Outer box | 2750 x 1 x 0.6 |

| 1,650 |

Direct Labour |

|

| |

One-way Switch |

|

| |

Un Skilled | 75 hrs x 100 | 7,500 |

|

Skilled | 15 hrs x 600 | 9,000 |

|

3 PIN Multiple Plug |

| ||

Un Skilled | 27.5 hrs x 100 |

| 2,750 |

Skilled | 5.5 hrs x 600 |

| 3,300 |

Machine Cost |

|

|

|

One-way Switch | 120 hrs x 400 | 48,000 |

|

3 PIN Multiple Plug | 44 hrs x 400 |

| 17,600 |

Fixed Cost |

| 3,00,000 | 1,10,000 |

Total cost | 1,21,125 | 70,125 | |

No. of units | 7,500 | 2,750 | |

Cost per unit | 16.15 | 25.50 | |

Add: Overhead | 0.25 | 0.25 | |

Final Cost per Unit | 16.40 | 25.75 | |

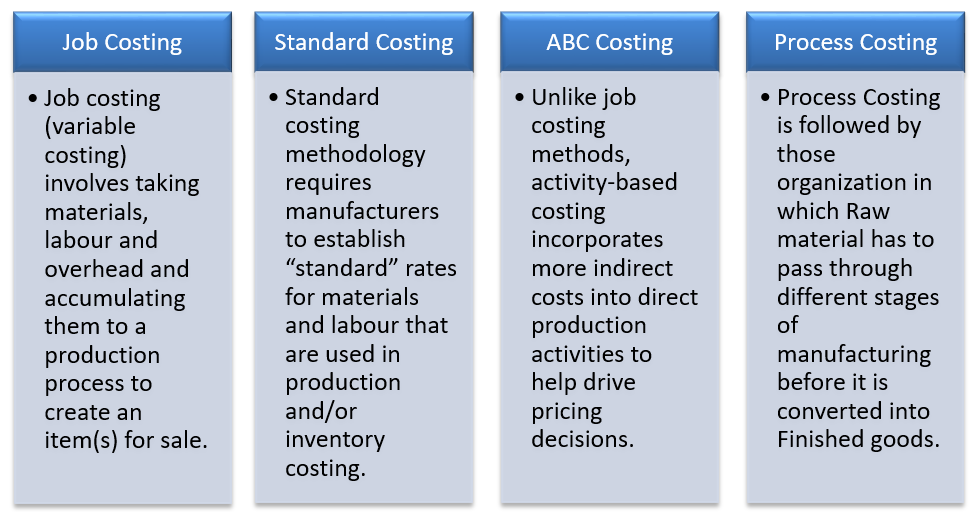

So, which costing model should manufacturers choose?

The costing philosophy/model that is best for a manufacturer is largely a cost-benefit relationship decision, and there really is no wrong answer if it makes sense for your business. For manufacturers that produce relatively few products, job costing may be a justifiable approach. For manufacturers that have a wider array of products or mass produce similar products, being able to directly associate costs to a specific product can be very difficult, if not impossible (at a minimum not worth the time and effort to attempt to achieve it). For them, standard costing or activity-based costing would likely be a better approach.

Regardless of which costing method works best, each has virtues that can help drive accurate pricing decisions.

III. Conclusion:

Determining appropriate costing helps to measure and develop competitive strategies which can be helpful to improve efficiency of internal operating processes. It provides basis for valuing manufactured inventory, Cost of Goods Sold (COGS) for external reporting and helps in making day-to-day decision. As significant and growing economic activity is being observed everywhere, Profitability needs to be improved with better understanding of the increased overheads, customer’s requirements, innovation and market condition for which costing is of great help. Costing helps to compare benchmarks, to provide cost causation and rational ascertainment of cost information for Managerial Decision Making. To conclude, costing system helps an organization to improve profitability, achieve organizational goals, target growth, sustainability and development.

Authors:

CA Aakash Mehta

Partner, MASD

E-mail ID: aakash.mehta@masd.co.in

Poojan Joshi

Associate Consultant, MASD

E-mail ID: poojan.joshi@masd.co.in

Sahil Rathod

Associate Consultant, MASD

E-mail ID: sahil.rathod@masd.co.in